Australia’s carbon and renewable energy markets moved again this quarter, and the latest Quarterly Carbon Market Report from the Clean Energy Regulator shows just how quickly storage, certificates and renewable supply are reshaping the landscape heading into 2026. For large C&I and multi-site organisations, the shift is well underway and the decisions around energy and carbon management are becoming more strategic.

Here’s what leaders need to know.

Battery Uptake Is Exploding – And It Changes Everything

Source: CER Quarterly Carbon Market Report, Figure 3.1

The Cheaper Home Batteries Program has moved faster than anyone expected.

- 175,000+ batteries expected by end of 2025 – delivering 3.9GWh of usable storage

- 54,000 batteries installed in Q3 alone

- Systems are getting larger, with average residential battery size rising from 16.6 kWh to 19.8 kWh across the quarter

This level of distributed storage is now larger than Australia’s five biggest grid-scale batteries combined, and could influence future reliability, price shape and the curve of minimum demand.

For business, this signals a future where aggregated household storage becomes a material part of system stability. This is a shift that will influence hedging costs, daytime pricing and the shape of evening peaks.

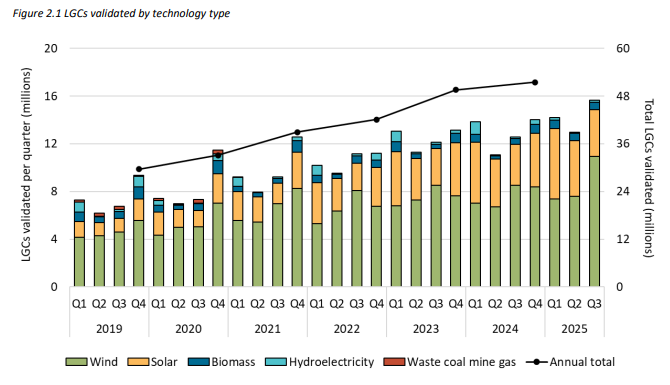

Renewable Supply Keeps Surging – Especially Wind

Source: CER Quarterly Carbon Market Report, Figure 2.1

Large-scale renewable generation set multiple records:

- 15.7 million LGCs created in Q3 – the highest quarter ever

- Wind contributed ~11 million LGCs, its strongest quarter yet

- Renewables reached 42.7% of generation in the NEM

- Total accredited capacity added in 2025 will be close to 7GW when combined with small-scale

Wind and solar output lifted materially from 2024, and grid-scale solar rose 16% year-on-year in Q3.

This strengthens the supply outlook but increases exposure to weather-driven volatility – a growing factor for retailers’ appetite, tender timing, and contract structures.

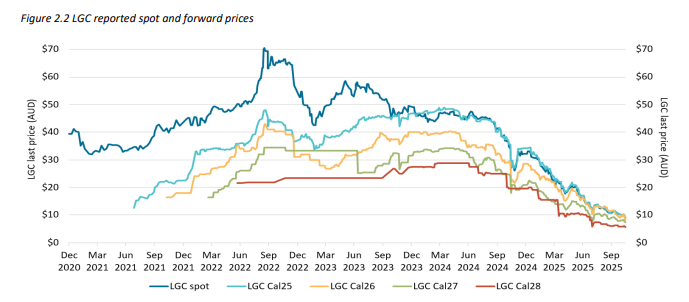

LGC Prices Have Fallen – Voluntary Demand Has Not

Source: CER Quarterly Carbon Market Report, Figure 2.2

Even with the highest supply on record:

- LGC spot prices fell from $16.50 to $10.80 in Q3, sitting at just $8.25 mid-November

- Yet voluntary cancellations hit 10.8 million by Q3 – already higher than the whole of 2024

Nearly half of all voluntary cancellations came from NGER reporters shifting to market-based scope 2 accounting.

Low prices are likely to drive more voluntary action in 2026 – good news for corporates aiming for 100% renewables, but a reminder that LGC procurement needs to be timed strategically.

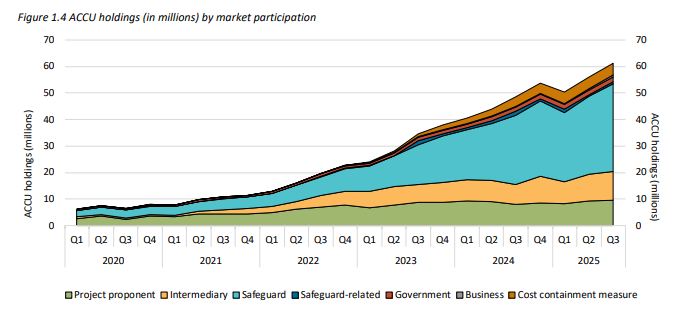

ACCU Market Tightening Continues

Source: CER Quarterly Carbon Market Report, Figure 1.4

Key movements in the ACCU and Safeguard Mechanism markets:

- 5.5 million ACCUs issued in Q3; year-to-date issuance of 15 million

- Total 2025 supply will likely fall in the upper range of 19–24 million

- ACCU holdings increased to ~57 million

- Safeguard facilities recorded a 2.4% cut in emissions year-on-year

- Entities exceeding baselines total 13.7 MtCO₂-e in potential excess

Most importantly, the ACCU price increased through the quarter, driven by safeguard entities consolidating holdings ahead of future declines in baselines.

Expect tighter ACCU markets later this decade as demand rises faster than supply.

New Certification Schemes Will Reshape Reporting

Two major integrity frameworks went live or advanced this quarter:

- Guarantee of Origin (GO) Scheme launched in November

- PGO (Product Guarantee of Origin): a new certificate that verifies how “low-emissions” a product is based on how it was produced.

- REGO (Renewable Electricity Guarantee of Origin): a new certificate for renewable electricity that will take over from LGCs once the Renewable Energy Target winds down.

- ACCUs have fully migrated to the new blockchain-based Unit and Certificate Registry, giving buyers transparency on method, location and issuance date

For businesses, this means more credible claims – but also more complexity in certificate procurement and reporting.

What This Means for Businesses

For many complex C&I organisations, the challenge isn’t the contract itself – it is timing, structure, retailer appetite and the moving parts around every decision.

The data from this quarter reinforces why strategy matters:

- Battery growth will change demand shape and peak pricing

- Large-scale renewable additions will influence forward curves

- Certificate markets are no longer predictable year to year

- ACCU tightening will drive long-term decarbonisation costs

- New schemes will make claims more transparent – and more scrutinised

With so many variables shifting at once – storage uptake, certificate prices, retailer appetite and compliance settings – the challenge for complex energy users isn’t the information or data itself, but knowing what to do with it.

That’s where Utilizer comes in. We interpret these signals and turn them into clear recommendations on timing, structure and risk so your decisions stay anchored, not reactive. Reach out and talk to one of our energy experts about your carbon and renewable certificate strategy for 2026.