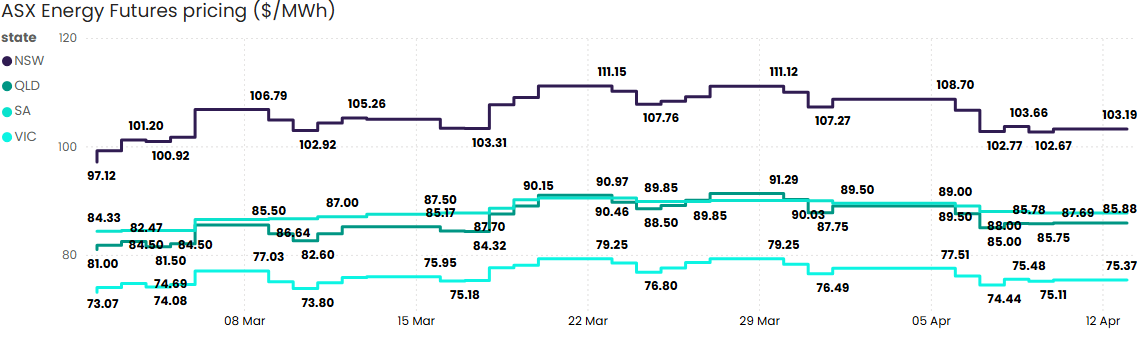

Australian energy markets have had an eventful six weeks. A surge in global fuel prices, a force majeure declaration from one of the world’s largest LNG exporters, and renewed Middle East tensions collided in early March to push electricity futures sharply higher – peaking through late March before easing briefly and recovering again into April. That pattern of spike, soften, recover tells you something important: this isn’t a market that’s settled. It’s one still working out what the new normal looks like.

⚡ Electricity Market

The catalyst was a pair of events that hit simultaneously and reinforced each other.

In early March, Qatar declared a force majeure on LNG exports. Qatar is one of the world’s top three LNG suppliers, and any disruption to its output tightens global gas supply quickly. Because Australian gas pricing is linked to international LNG markets through the netback mechanism, higher global prices make it more expensive to keep gas onshore. And that flows through to gas-fired electricity generation costs.

Around the same time, Newcastle thermal coal prices surged 35% to around US$135 per tonne. Coal-fired generation still sets marginal electricity prices across much of the NEM, particularly in NSW and Queensland. When the cost of coal moves that sharply, forward electricity prices follow.

It’s worth noting the timing. The AER’s draft Default Market Offer for 2026-27, released in mid-March, had pointed toward potential retail price reductions based on pre-conflict wholesale costs. Those outcomes are now uncertain. Businesses who were expecting relief on their next contract or retail bill may need to factor the changed forward curve into their thinking.

Q2 2026 futures rose sharply across all NEM regions through late March. Prices softened briefly as Middle East tensions showed early signs of easing before recovering through April. It’s a pattern making procurement conditions more challenging and retailer pricing windows shorter.

There’s a broader tension playing out in the market right now: renewable generation and battery storage continue to suppress average spot prices, while geopolitical risk is simultaneously lifting the forward curve. Those two forces are pulling in opposite directions, and how that resolves will shape procurement conditions for the rest of 2026.

Source: ASX Energy Futures

🔥 Gas Market

Gas tells a different story to electricity right now, and understanding the gap between them matters.

Across the east coast, gas prices fell through the quarter. AEMO has identified improved near-term supply conditions, with risks of extreme peak day shortfalls in NSW, SA and VIC now expected to emerge a full year later than previously forecast. Two things are driving that improvement: the temporarily delayed retirement of Eraring Power Station is reducing reliance on gas-fired peaking generation, and APA’s committed expansions to the north-south pipeline system are improving access to northern supply for southern markets. Battery storage uptake across the NEM is also eating into peak gas demand.

That structural improvement is real, but it doesn’t eliminate near-term seasonal risk. Iona underground storage, which plays a critical role in meeting peak winter demand across the southern states, ended 2025 at its lowest level since 2021. Combined with the ACCC’s forecast of a potential shortfall of up to 8 petajoules in Q3 2026 depending on LNG exporter behaviour, Victorian and South Australian buyers in particular face heightened winter price risk if conditions tighten through the colder months.

Source: AEMO STTM and DWGM

🌏 LNG Netback

Don’t let the soft domestic gas numbers lull you into thinking the gas story is straightforward. It’s not.

To understand the scale of what’s shifted, some context helps. The disruption to Hormuz shipping in early March effectively removed around 14% of global monthly LNG supply in a single month, with Asian spot prices surging around 65% as a result. Australia, as one of the world’s largest LNG exporters, is directly exposed to that repricing dynamic through the netback mechanism. The doubling of forward netback expectations from January’s outlook isn’t a gradual revision. It’s a structural reset driven by a genuine supply shock.

The LNG Netback price is effectively the floor that international demand sets for Australian gas. When it rises this sharply, it pulls domestic contract pricing upward over time regardless of what’s happening in local spot markets. The current east coast gas softness is real, but it may be shorter-lived than the supply picture currently suggests.

For businesses with gas contracts expiring in the next 12 to 18 months, or electricity exposure linked to gas-fired generation, this is the number worth understanding before your next procurement decision.

💧 New Zealand

The NZ wholesale electricity market swung dramatically over the period, with prices rising more than 200% from February to March before showing early signs of softening in April. The scale of the move is worth understanding, because it wasn’t driven by the same fuel cost pressures affecting Australian markets.

New Zealand’s generation fleet is around 80% renewables, predominantly hydro. That’s a structural advantage in normal conditions, but it creates acute vulnerability when storage lakes run low. Tightening hydro storage through late summer was the primary driver of the price spike, compounding the broader global energy market volatility stemming from Middle East tensions.

The practical consequence was that gas and coal-fired thermal generation, which NZ keeps in reserve for exactly these conditions, was called on heavily to fill the gap. That drove costs sharply higher across the wholesale market before storage conditions began to stabilise heading into April.

For Australian businesses with operations or energy exposure in New Zealand, the episode is a useful reminder that energy risk doesn’t always come from the direction you’re watching. A market that looks structurally clean can reprice dramatically when its single point of vulnerability is tested.

👀 What We’re Watching

The doubling of forward netback expectations from January’s outlook is the most significant structural signal in this month’s data. We’re watching whether the step-change in LNG netback puts upward pressure on domestic contract negotiations, particularly for businesses approaching renewal in the second half of 2026.

Electricity futures have shown they can move sharply and quickly in response to global events. Retailer pricing behaviour has shifted noticeably. Validity windows have tightened and the market has become more reactive as forward curves move. Whether conditions stabilise through Q2 or remain volatile depends largely on how the geopolitical situation develops.

The delayed retirement of Eraring Power Station is providing near-term gas demand relief, but it’s a temporary buffer. As coal-fired capacity continues its longer-term exit from the NEM, structural pressure on gas and storage will return. Businesses planning energy strategy over a two to three year horizon should be factoring that trajectory in now.

The December 2025 Gas Market Review recommended a formal domestic gas reservation scheme requiring 15-25% of production to be supplied to the domestic market, replacing the existing heads of agreement and price cap arrangements. Consultation is underway in 2026 with implementation targeted for 2027. For businesses negotiating longer-term gas contracts, this is a policy shift worth monitoring closely.

If any of these are relevant to your current contracts or upcoming procurement decisions, get in touch. Our team is across the market and ready to help you make sense of what’s shifting.

Frequently Asked Questions

Gas prices are falling but my electricity bill isn’t. Why? +

Electricity and gas pricing are driven by different dynamics. East coast gas spot prices have softened due to improved local supply conditions, but electricity forward markets are reacting to global developments, rising coal prices and LNG export disruptions, that push generation costs higher regardless of what’s happening in the domestic gas spot market. The two don’t always move together, and right now they’re telling very different stories.

What does the Qatar force majeure actually mean for Australian businesses? +

Qatar is one of the world’s top three LNG exporters. When it declares a force majeure, it means supply commitments can’t be met and global gas markets tighten quickly as buyers scramble for alternative sources. Australia’s east coast gas market is linked to international LNG pricing through the netback mechanism, so when global prices rise, the cost of retaining gas domestically rises with it. That pressure flows through to electricity generation costs too.

Should I be locking in a contract now or waiting for prices to soften? +

Timing the market is rarely the right frame for this decision. What matters more is whether you’re procurement-ready, meaning your site data is current, your portfolio is organised, and you can move quickly when conditions shift. The LNG netback step-change suggests the current window of relatively soft gas pricing may not last. If your contract is expiring in the next 12 to 18 months, the more important question is whether you’re positioned to act when an opportunity appears.

Why are retailer pricing windows getting shorter? +

When forward markets are moving quickly, retailers face real exposure between the moment they issue a price and the moment you accept it. In volatile periods, that gap becomes commercially risky, so they shorten validity periods to limit how long they’re locked into a price that may no longer reflect market conditions. For buyers, this means you need to be able to evaluate and respond to offers faster than you might in a stable market.

Is Victoria actually a safer market for energy buyers right now? +

Victoria recorded the smallest price increase of the four NEM states this period, up just 3.1%, and continues to sit at the lower end of the NEM pricing curve. A more diverse generation mix and stronger interconnection have provided some insulation. But VIC is still moving in the same direction as every other state, driven by the same underlying forces. Relative stability isn’t the same as immunity from market pressures.

What’s the Eraring retirement, and why does it matter beyond NSW? +

Eraring is Australia’s largest coal-fired power station, located in NSW. Its planned retirement has been temporarily delayed, which in the short term is reducing the NEM’s reliance on gas-fired peaking generation. For southern states, this has helped ease near-term gas demand pressures. But it’s a delay, not a cancellation. When large coal capacity does exit the NEM, the pressure on gas and storage will return, which is why businesses planning over a multi-year horizon need to keep that trajectory in view.